Secure Your Future with Smart Finance

Market Downside Protection

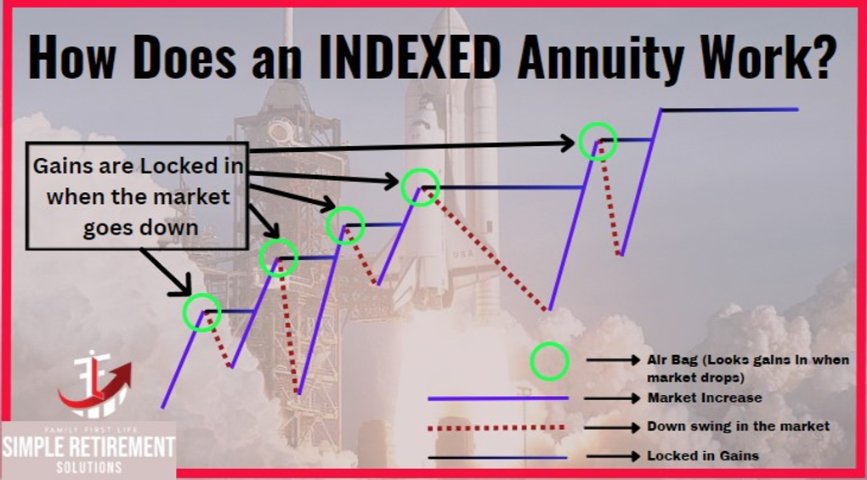

How It Works

- Fixed Annuities: Provide a guaranteed rate of return regardless of market conditions. The insurance company assumes the investment risk, ensuring that the annuity holder receives a consistent income stream.

- Variable Annuities with Riders: Allow investments in sub-accounts that can fluctuate with the market. To protect against downside risk, these annuities offer optional riders like the Guaranteed Minimum Income Benefit (GMIB) or Guaranteed Minimum Accumulation Benefit (GMAB), ensuring a minimum payout even if the underlying investments perform poorly.

- Indexed Annuities: Tie returns to a market index (e.g., S&P 500) but typically offer a guaranteed minimum interest rate, ensuring that the principal is protected even if the index performs poorly. Gains are capped at a certain percentage to balance the insurer's risk.

Life Insurance

- Whole Life Insurance: Offers a guaranteed cash value accumulation component. The insurer manages the investment risk, providing stable growth of the policy's cash value.

- Universal Life Insurance with Secondary Guarantees: Provides a flexible premium structure and the potential for cash value growth based on market performance. Secondary guarantees ensure that the death benefit remains intact as long as certain conditions are met, regardless of market performance.

- Variable Universal Life Insurance with No-Lapse Guarantees: Allows policyholders to invest in various sub-accounts with market exposure. No-lapse guarantees ensure that the policy remains in force even if the market performs poorly, provided certain premium and funding requirements are met.

Insurance vs. Investment Accounts

Insurance Products

Investment Accounts (401(k), IRA)

| Feature | Annuities and Life Insurance | 401(k) and IRA |

| Principal Protection | Yes (through guarantees) | No |

| Guaranteed Income | Yes (for annuities) | No |

| Market Exposure | Limited (indexed and variable products) | Direct |

| Potential Returns | Typically lower due to caps and fees | Potentially higher due to direct market exposure |

| Death Benefit | Yes | No |

| Investment Flexibility | Limited (set by insurer) | High (wide range of investment options) |

| Risk | Lower (due to guarantees) | Higher (market-dependent) |

Social Security

How Social Security Works

- Funding Source:

- Trust Funds:

- Benefit Calculation:

- Adjustments and Cost-of-Living Adjustments (COLAs):

Stability and Protection

Comparison to Market Downside Protection

| Feature | Social Security | Market Downside Protection in Annuities/Life Insurance |

| Market Exposure | None (invested in Treasury securities) | Some (depending on product type) |

| Government Backing | Yes | No (backed by private insurers) |

| Principal Protection | Yes (through Treasury securities) | Yes (through guarantees and riders) |

| Inflation Protection | Yes (through COLAs) | Varies (some products offer inflation protection) |

| Income Guarantee | Yes (lifetime benefits) | Yes (for certain annuities) |

4% Safe Withdrawal Rate vs 7% Payout Rate

| Variable Products | Indexed Products |

| Stock Market Accounts: Any savings product subject to the ups and downs of market volatility. | Typically, Annuities whose growth is tied to a popular stock market index, but is not invested in it. |

| Brokerage Accounts: 401k, Mutual Funds | Annuities, Index Universal Life Insurance (IUL) |

| 4% Withdrawal Rate | 6-8% Payout Percentage |

| Typically calculated towards a 30-year retirement savings account starting at age 65 | Typically calculated towards a Maturity date age (age 99 for annuities & age 120 for life insurance) |

Key Concepts of Safe Withdrawal Rate (SWR)

Portfolio Composition:

Factors affecting SWR

Swiss Retirement System

| Assets: $500,000 | |

| Annual 4% Safe Withdrawal Rate | $20,000/year |

| Annual 7% Payout Rate | $35,000/year |

| Difference per year | $15,000/year |

| Difference after 10 years | $150,000 |

| Difference after 30 years | $450,000 |

Individual

IRA (Individual Retirement Account)

Key Differences:

Tax-Free

| Tax Free Accounts |

| Roth IRA |

| Indexed Universal Life Insurance |

| Whole Life Insurance |

Tax Deferred

| Tax Deferred Accounts | |

| 401k | 403b |

| 457b | IRA |

| SEP IRA | Simple IRA |

Disadvantages of Market Loss for, Investment Retirement Accounts

Other Risks and Disadvantages

Our Solutions

Utilize the Swiss Formula combined with a Death Benefit (Cash Value) to optimize your retirement income. As detailed in the 4% safe withdrawal rate versus 7% payout comparison , this approach allows you to achieve higher income from the same assets.

Key Benefits

By leveraging the Swiss Formula, you can enjoy a higher payout from your assets compared to traditional methods.

Unlike annuitization, this strategy ensures that you retain your assets, providing financial security and flexibility.

Your beneficiaries receive a death benefit, ensuring their financial stability.

The accumulated cash value can be used for investments or to cover extraordinary expenses, offering additional liquidity and financial planning options.

Why choose this Approach?

How We process:

Option #1 Transfer

Option #2 Rollover

Rollover to an IRA (Individual Retirement Account)

- Traditional IRA: You can roll over your 401(k) funds to a Traditional IRA without paying taxes. This option offers a wider range of investment choices compared to most 401(k) plans.

- Roth IRA: If you choose to roll over to a Roth IRA, you'll have to pay taxes on the rollover amount since Roth IRAs are funded with after-tax dollars. However, future withdrawals in retirement can be tax-free.

Partial Rollover

- Mix and Match: You can roll over part of your 401(k) to an IRA or new employer's plan while keeping the rest in the old plan.

- Benefits: Flexibility to take advantage of different investment opportunities and manage your tax liabilities.

- Considerations: Requires careful planning to manage accounts and avoid unnecessary fees.

In-Service Rollover

- Age Requirement: Most 401(k) plans allow in-service rollovers once you reach the age of 59½. This age threshold is important because it’s the point at which you can take distributions from your 401(k) without incurring a 10% early withdrawal penalty.

- Plan-Specific Rules: Not all 401(k) plans offer in-service rollovers. You'll need to check with your employer or plan administrator to confirm whether your plan allows it and what the specific requirements are.

- Traditional IRA: You can roll over your 401(k) funds to a Traditional IRA without any tax implications. This gives you access to a broader range of investment options and potentially lower fees.

- Roth IRA: Rolling over to a Roth IRA is also an option, but you will owe taxes on the rollover amount since Roth IRAs are funded with after-tax dollars. Future withdrawals from a Roth IRA are tax-free, which could be advantageous in retirement.

- Partial Rollover: You might choose to roll over only a portion of your 401(k) balance, leaving the rest in your employer's plan.

- Diversification and Investment Control: IRAs typically offer a wider variety of investment options compared to many 401(k) plans. This allows for greater diversification and the ability to tailor your investments to your specific retirement goals.

- Lower Fees: IRAs often come with lower administrative fees than employer-sponsored 401(k) plans, which can result in cost savings over time.

- Tax Planning: If you anticipate being in a lower tax bracket in the future, rolling over to a Roth IRA and paying taxes now might be beneficial.

- Estate Planning: IRAs can offer more flexible beneficiary options than 401(k) plans, which may be important for your estate planning needs.

Option #3 Open a Retirement Savings Account

- Tax Treatment: Contributions may be tax-deductible, and the account grows tax-deferred. Taxes are paid upon withdrawal during retirement.

- Eligibility: Available to anyone with earned income. There are no age limits to contributions, but there are income limits for tax-deductibility.

- Tax Treatment: Contributions are made with after-tax dollars, and the account grows tax-free. Withdrawals during retirement are tax-free.

- Eligibility: Available to individuals within certain income limits. Contributions are limited based on your filing status and modified adjusted gross income (MAGI).

- For Self-Employed or Small Business Owners: Allows employers to contribute to employees' retirement savings. The employer can contribute up to 25% of each employee’s compensation.

Business

- Contributions are typically made with pre-tax dollars, reducing taxable income.

- The money grows tax-deferred until withdrawal.

- Employers can deduct contributions made to these plans from their taxes.

- 401(k) Plans

- 403(b) Plans

- 457(b) Plans

- Traditional Defined Benefit Pension Plans

- Deferred Compensation Plans

- Executive Bonus Plans

- Supplemental Executive Retirement Plans (SERPs)

Key Differences:

In collaboration with our partners, we offer a range of services to implement a new employee retirement plan or reorganize your existing one.